Now that the indy debate has devolved from professionals to real people it has become muddier. All sorts of voices are chiming in with their two cents’ worth—as it should be. But over the last month as the babble has intensified, Clarity has been the first casualty. Folk—rightly—have a broad range of opinion; falling into the lock-step of a single voice is not human nature.

Unfortunately, truth has not been far behind in getting wheeled into A&E. While the vast bulk of these new voices are undoubtedly sincere, there are more than a few on the payroll vote stirring it and some amazingly gallus slants put on various news items by a media that will be pilloried at sopme point in the future for falling down on their prime duty: objectivity.

But, as hardened observers of the Fifth Estate will long have practiced, a strong filter of their own research, familiarity with the pundit in question and a healthy dash of skepticism does much to focus the truth, much as a projector lens throws a clear image on a screen—if properly set up.

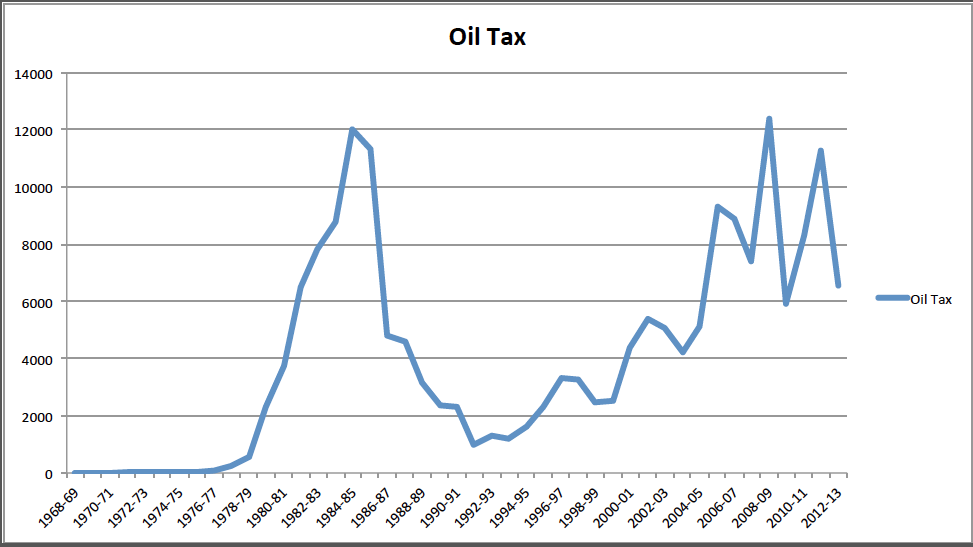

This week, the turd in question arriving at the fan blades were the GERS figures for last year. Although they didn’t make front page in the Cornish Guardian, from the Rhinns Reader to the Yell Yeller, it became the talk of the steamie that oil tax revenues for HM Treasury fell from £10bn to £5.6bn from the previous year and that ~Scotland’s fiscal public deficit shifted thereby from being better than the UK average of 7.3% to a rather worse 8.3%.

Let’s leave to one side whether any treasury mandarin cooked these books. Tax revenue does fluctuate and such numbers are plausible and would have to be dealt with by an independent Scottish Treasury. But is it, as Labour Finance Spokesman Iain Gray almost had a heart attack running between channels to tell us, proof that Scotland should stay in the UK? Are oil revenues in ten, as opposed to eleven digits, bad news?

Iain, for one, needs to have a word with himself. Serious financial trends are never predicted from one set of figures—certainly not without reading the small print. Some £2bn of the drop this year were due to a larger figure being invested in the North and Celtic Seas and the justifiable tax incentives for our future kicking in. Then there is the fact that last year was a rather good year and bucked the general trend of gentle decline in the figures. In fact, looking back a decade or two, it’s easy to see why even sober, neutral commentators caution against over-dependency on such a volatile revenue source.

Total Treasury Revenues from Oil & Gas by Year in £m. (Source: HM Treasury)

So, not only are fluctuations pretty much the norm but the UK Treasury has suffered considerably lower annual incomes 1990-95 without their fiscal world coming to an end. Ah, retort the unionist apologist rentaquotes like Iain; that’s because the UK economy is so much bigger and provides exactly the ‘flywheel’ effect we need. He rather ignores that Norway, rather than squandering £165bn so far as the UK has done, built up a quarter trillion ‘oil fund’ to act as their flywheel—and to gain a quarter of their income from interest from it as a side effect. Some ‘side effect’.

The other point that Iain gamely makes is that it now costs twice as much to extract each barrel than it once did. Quite true and—as we drill deeper and further out—likely to get worse. What Iain’s highly selective grasp of figures fails to mention is that firms are falling over themselves to spend that extra money because the higher price of oil makes it very much worth their while—indeed many overheads become proportionately less of a burden.

Historic Global Crude Oil Prices by Year in $US/barrel (Source: Macrotrends)

This shows price history back to the two dramatic leaps in the 1970’s. The average price over these 45 years has been $40. The current price of $100 (with an obvious steady upward trend if the 2008 ‘blip’ is removed) means that, despite a doubling in cost, there is now a 50% extra profit margin available to companies, as compared to historic average—and that seems likely to increase. Fold into the equation the fact that half the oil remains to be extracted (at these or higher prices) and it may be time for Iain to upgrade his crystal ball and/or trade in his slide rule if he is to be current.

It’s probably unfair to pick on the unfortunate Mr Gray who is strapped into the job of mouthpiece for a party that embodies the scene from Life of Brian in which a streetful of people all chant “Yes, we must all learn to think for ourselves“. Much more relevant are comments from business leaders who have less of a posturing and more of a pragmatic role they are following—as often as not with the interests of their business to the fore.

This week at their annual conference Stephen Leckie, chair of the Scottish Tourism Alliance, said there was huge uncertainty for what independence would mean for his £11bn industry that employs over 200,000 people. In particular:

“The discussions and debates and arguments that are going on at the moment are, I think, not representing Scotland and the parliament well. All it is is everyone just arguing with each other.”

He has a fair point. The problem with providing figures he (and many others) say are missing from the White Paper is no party has ever provided detailed financials prior to any election. With the UK digging heels in over whether the £UK could be shared, so many imponderables are created that even making a stab at Scotland’s would be a fool’s errand.

On the other hand, world-leading maker of portable power supplies Aggreko’s CEO Rupert Soames waded into the debate claiming that his business was being damaged by uncertainty from debate over independence. Sounds plausible—until you realise that this is Winston (Empire-is-my-Life) Churchill’s grandson and brother of Tory Minister Nicholas Soames. Having lobbed his grenade, he promptly resigned to run Serco “The Company that Runs Britain” since accused of so fraudulently over-charging on contracts to tag criminals such that the UK government has banned them getting any new work. Meanwhile, Aggreko share price dropped by 9%. Nice.

Probably most significant are the rumblings from Scotland’s £17bn/150,000-worker finance sector that they may have to consider their staff and HQ deployments in the even of independence. Scottish Widows, RBS, Standard Life and BoS wing have all been quoted in this context. These seem to be both genuine and sensible for such firms. Nobody—least of all the Scots—want to see any of them go. But, before unionists expect us all to head screaming for the hills at the prospect, we should bear in mind what is meant by ‘go’.

Both Standard Life and BoS are already part of the Lloyd’s group, which has the bulk of its staff and business outside of Scotland. Important though their operations are here, it is hard to see either being disrupted by major moves of staff south—especially when office space in Canary Wharf (at £55/sq.ft.) is more than three times that of the Gyle (£16/sq.ft.). Standard Life, being listed on the London stock exchange, is less of a Scottish company than it used to be. As for the Royal Bank of Scotland, it is these days largely a Scottish company in name only.

Standard Life has previous form in these matters. As long ago as 1992 it warned that devolution – never mind independence – might cause it to relocate south of the border. Well, devolution happened and Standard Life is still here. As for RBS, Mark Carney told the Treasury select committee that an independent Scotland would have to guarantee deposits held in England by Scottish-domiciled banks under EU law and so could lead to RBS HQ moving to England. But three facts modulate the impact of any such move:

- Just where the company displays its brass plate involves a hundred or so staff at most; BoS HQ remains a spectacular but nonetheless small building on the Mound

- The bulk of operations and therefore staff and therefore economic advantage would remain wherever they are now.

- Removing the HQ of such global giants removes the main argument against currency union as the bank of last resort connection would move with the HQ, unburdening the new Scottish Treasury.

Nobody sensible objects to all companies making contingency plans—which explains 90% of the fluff spun by the press over the last month. What has received rather less coverage and speculation is the possible good news story from independence if:

- Oil tax revenues average over £8bn—as they have for the last decade?

- Scotland puts its £2bn annual saving from defence (alone) into its own oil fund?

- Oil continues to rise at ~$5 each year, boosting tax revenue to £12bn by 2025?

- Whisky exports continue to grow past the £4bn p.a. already achieved?

- Renewables employment exceeds last year’s 5% growth (to 11,365 people)?

- Tourist expenditures grows better than the 15% achieved in recent years?

Funny, but unionists and their media never seem to think of bringing up such possibilities.