Norwegian Air Shuttle (NAS) started small. It was founded on 22 January 1993 from the bankrupt wreckage of Norwegian regional airline Busy Bee by 50 then-redundant former employees. Using three Fokker 50 aircraft, they contracted with Braathens to link the scattered cities on Norway’s west coast. For the next decade, they grew steadily and profitably on this basis until SAS took over and absorbed Braathens, unilaterally cancelling contracts that should have been given 18 months’ notice.

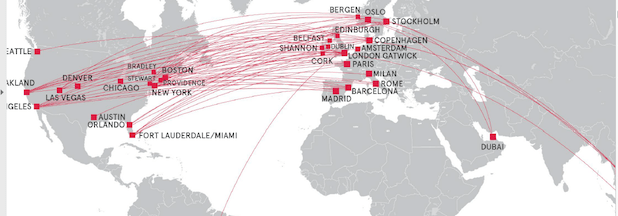

Norwegian shrugged off this setback by re-purposing its fleet of MD-80 short-haul jets to become a low-cost carrier between Scandinavia and Eastern Europe. This was reinforced by their 2007 purchase of FlyNordic from Finnair. That same year, they ordered 42 Boeing 737s and their fleet of these had grown to 78 by 2011. By then, they had started leasing the new Boeing 787 Dreamliners for long-distance use between Europe and both west coast USA and the Far East.

Such a massive expansion was made possible by significant restructuring and creative financing, including sale and lease-back of much of its fleet. The spectacular growth has been led by by CEO and largest shareholder Bjørn Kjos, Under the control of Norwegian Air Shuttle ASA is a bewildering variety of associated subsidiaries. The group’s revenue passed £1bn in 2015 and has grown since—nu 30% in 2017. In its 26 years, it has grown to be the ninth-largest low-cost airline in the world.

It has managed to do this by luring passengers away from both conventional and low-cost airlines in Europe and by competing very effectively on long-haul routes—especially to North America—by bringing low-cost competition to airlines like BA. Not only does Norwegian undercut them on price but the Dreamliners used are faster, quieter and more comfortable than BA’s fleet of aging 747 Jumbos. But this growth has come at a cost. Net profit in 2017 was a loss of around £100m, although it is difficult to be precise because of the flurry of operations run through subsidiaries. Although the stock trades on the Oslo exchange with an EPS ratio round 9, the stock value has halved since its peak of NOK 377 in 2015. (£1 ~11Norwegian Kroner). NAS’ capital structure shows ratio of its debt to equity stands at a dangerous level over 1,000 to 1.

By last summer, the financial gnomes of Canary Wharf and Wall Street had written NAS off as good to invest in only in hopes of a takeover by some other airline. Those in the know were advising friends not to book with Norwegian, in case they found themselves stranded. But NAS has flown on into the winter, paying its bills and keeping its vast network of routes carrying over 30m passengers during 2018. Even the Wall Street Journal admitted that (to paraphrase Mark Twain) rumours of its death had been greatly exaggerated.

This not to say it won’t suddenly go the way of once-leading airlines like Pan Am, Laker, TWA or BMI in this highly competitive field. But if you don’t mind flying via Gatwick or Copenhagen, you can find deals under £200 to Los Angeles, Las Vegas or San Francisco you might consider worth the risk. I would.

Disclosure: I have no stock nor have any financial interest in NAS, or its subsidiaries. I have flown with them five times, finding the flights comfortable and punctual…but the staff training—both on the ground and in the air—was inadequate.